October 2025 Monthly Housing Market Trends Report

- Inventory climbs but growth slows: Active listings rose 15.3% year over year, marking the 24th straight month of gains. However, the pace of growth has eased each month since May, signaling a plateau in the post-pandemic inventory recovery.

- Regional divide has begun to narrow slightly: Inventory growth in the South and West has slowed since spring, offsetting modest gains in the Northeast and Midwest and stalling the national recovery.

- Buyer activity remains soft despite lower mortgage rates: Even as rates have fallen to 12-month lows, homes are spending longer on the market for the 19th straight month (63 days, +5 YoY). Pending sales slipped 1.9% YoY.

- Prices hold steady nationally but fall in the South and West: The national median list price edged up 0.4% YoY to $424,200. The price per square foot dipped 0.5% YoY, with declines in the South and West and gains in the Northeast and Midwest.

- Shutdown weighs on buyer confidence and housing activity in federal metros: Early data shows dips in new listings and search activity in Washington, DC, Virginia Beach, Oklahoma City, and Baltimore—markets with the highest shares of federal employees. Broader price and inventory trends, however, remain largely unchanged for now.

In October, homebuyers saw more options as inventory grew for the 24th consecutive month, according to Realtor.com® housing data. The number of homes for sale remained above 1 million for the sixth month in a row, but the pace of growth continued its slowdown that began in mid-summer.

Despite falling mortgage interest rates over the past few months, the housing market’s pace remains slow. Homes spent longer on the market for the 19th straight month, with the slowdown most pronounced in Florida and the West. List prices nationally were flat year over year but slipped in the South and West, with regional differences starker when measured on a per-square-foot basis.

This month’s report also takes a closer look at how the federal government shutdown is playing out across local housing markets. Using new data on early signs from Realtor.com® listings and search activity, we find that housing markets with the highest shares of federal employees—such as Washington, DC, Virginia Beach, Oklahoma City, and Baltimore—are showing early signs of a pause in some housing market activity. New listings and buyer searches have slowed the most in these metros as uncertainty around paychecks weighs on confidence, even as broader market trends remain largely unchanged.

Table of Contents:

- Inventory: Active Listings and Regional Breakdown

- Flows: New and Pending Listings

- Momentum: Time on the Market, List Prices, Price Reductions

- In Focus: Government Shutdown and Local Housing Markets

- Data Appendix

Taking Stock: Buyers Gain Options, but Inventory Growth Slows

Homebuyers found more options in October, as the number of actively listed homes rose 15.3% compared to the same time last year. While this marks the 24th consecutive month of year-on-year inventory gains, active listing growth has slowed in each of the past five months (down from 17% in September, 20.9% in August, 24.8% in July, 28.9% in June, and 31.5% in May). The number of homes for sale topped 1 million for the sixth consecutive month, unchanged since July.

Still, nationwide October inventory remains 13.2% below typical 2017–19 levels, about the same as last month, an indication that the nationwide inventory recovery has stalled.

Where housing inventory is growing the fastest

Inventory increased in all four major U.S. regions in October, but the pace of that growth has slowed recently.

- West: +17.4%

- South: +17%

- Midwest: +12.2%

- Northeast: +8.9%

At the metro level, all of the 50 largest markets recorded year-over-year inventory growth. These metros saw the sharpest increases:

- Washington, DC* (+38.2%)

- Charlotte (+36.4%)

- Las Vegas (+35.1%)

Where housing inventory has recovered since the COVID-19 pandemic

For October, inventory in the West (+3.2%) and South (+4.6%) remains above pre-pandemic norms, while the Midwest (-35.7%) and Northeast (-48.6%) continue to lag significantly. At the national level, recovery vs. pre-pandemic has effectively stalled—largely driven by the relative slowdown in the West, where inventories this summer were as large as 11.4% above pre-pandemic norms.

At the metro level, 10 of the top 50 metros now exceed their pre-pandemic inventories by 25% or more—all in the South or West. These markets continue to have the greatest inventory relative to their pre-pandemic levels:

- Denver (+57%)

- San Antonio (+51.9%)

- Austin (+44.9%)

Flows Slow: A Look at New and Pending Listings

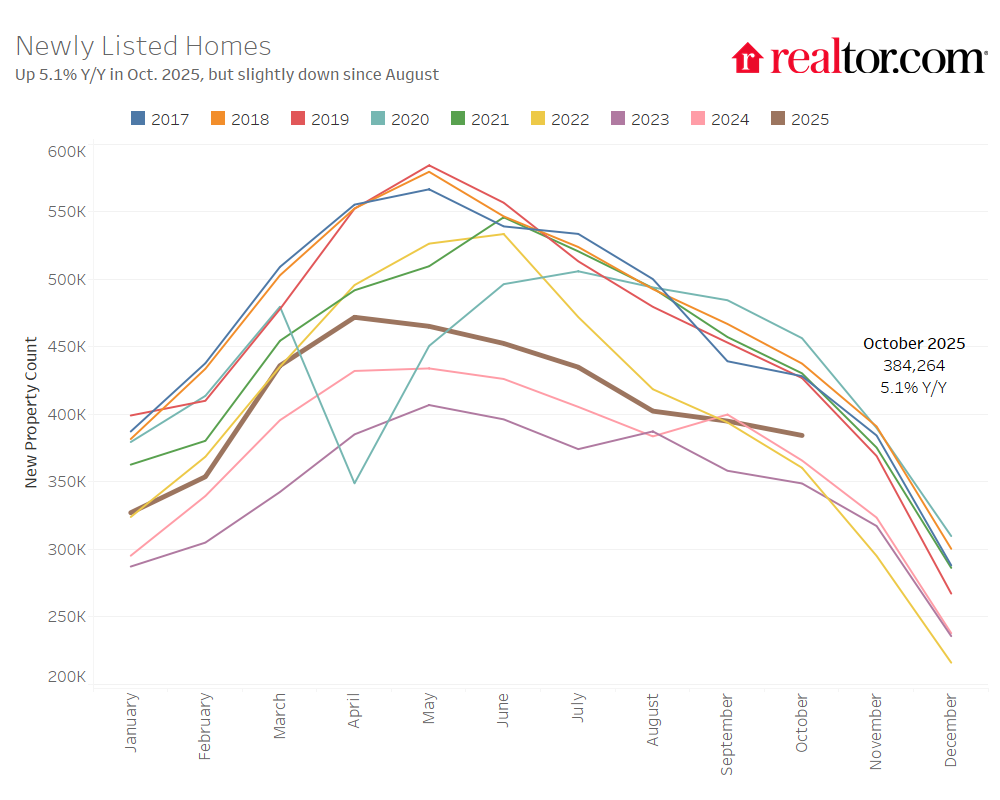

Newly listed homes grew 5.1% year over year, and were down 2.7% month over month, roughly in line with seasonal trends. New listings in October were 19% below their 2025 peak from April, but the pace of the decline has slowed since August.

On an annual basis, newly listed homes increased in all four regions:

- Northeast: +3.3%

- Midwest: +4.8%

- South: +5.2%

- West: +4.2%

While inventory was up, buyer activity was more subdued. Pending home sales—listings under contract—fell by 1.9% year over year, returning to negative territory after a flat reading in September.

See Appendix for pending sales figures

Gauging Momentum: Prices Remain Near October Peaks Despite a Slowing Pace

In October, the typical home spent 63 days on the market, which is 5 days longer than the same time last year. This marks the 19th straight month of homes taking longer to sell on a year-over-year basis. However, the gap has shrunk, falling below the one-week mark for the first time since June. With a median of 63 days, homes are now selling 3 days faster than their October 2017–19 norms after pacing in line with pre-pandemic norms in July through September.

In short, time on the market has returned to more historically normal levels, although inventory still lags.

Regional and metro trends: Time on the market keeps on ticking

- West: +8 days

- South: +5 days

- Midwest: +2 days

- Northeast: +2 days

Relative to pre-pandemic norms, only the West is seeing slower sales:

- West: 11 days slower

- South: 1 day faster

- Midwest: 14 days faster

- Northeast: 19 days faster

Among the 50 largest U.S. metro areas, just 3 saw homes move faster than last year: Providence, St. Louis, and Minneapolis. Longer time on the market remains a key contributor to the widespread year-over-year increases in active inventory. These metros saw the biggest slowdowns in time on the market:

- Miami (+13 days)

- Orlando (+12 days)

- Denver (+11 days)

List prices remain flat nationally, but fall slightly in the South and West

In October, the national median list price was $424,200, up 0.4% from last year and down a touch (-0.2%) since last month. The price per square foot fell slightly (-0.5% YoY and -0.8% MoM).

Since October 2019, the typical list price has climbed 36.9%, while the price per square foot is up 49.8%. Since October 2022, the national median list price is -0.2%, while the price per square foot is +3%—despite a 46.1% increase in inventory and the median home staying on the market for 13 days longer.

Regional list price patterns: Overall vs. per square foot

- Median list price YoY: Northeast 0%; Midwest +0.8%; South -0.9%; West -2.6%.

- Price per square foot YoY: Northeast +3.8%; Midwest +1.1%; South -1.4%; West -1.6%.

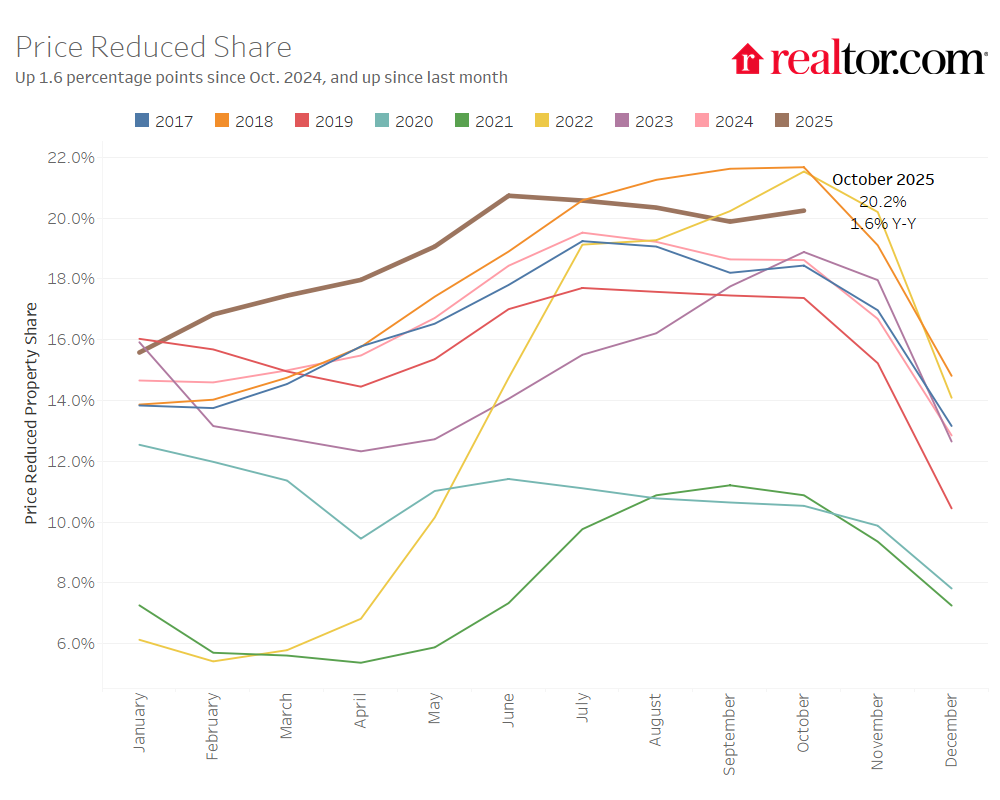

Price cuts remain elevated

In October, 20.2% of home listings had price reductions—up 1.6 percentage points from last year, and up slightly since last month. Price reductions in October have begun to show more uniformity by region (around the national average), though the Northeast is an exception with price cuts on less than 15% of listings.

These metros saw the most listings with price cuts, often linked to slower demand:

- Denver (31.3% of listings)

- Portland (31.1%)

- Indianapolis (30.9%)

In Focus: Government Shutdown and Local Housing Markets

Using new data on where federal workers live and early signs from Realtor.com® listings and search activity, we find that housing markets with the highest shares of federal employees—such as Washington, DC, Virginia Beach, and Baltimore—are showing early signs of a pause in housing activity. New listings and buyer searches have slowed in these metros as uncertainty around paychecks weighs on confidence, even as broader market trends remain largely unchanged.

The federal government shutdown that began on Oct. 1 and continues as of this writing has halted many public services and created uncertainty for hundreds of thousands of federal employees. Much has already been written about how the shutdown could affect the housing market—from delayed mortgage processing and halted flood insurance renewals to paused economic data releases that shape mortgage rate expectations.

This month’s special angle looks at the geography of the shutdown by analyzing how local housing markets with larger shares of federal workers are feeling the impact. To capture very recent shifts in listings, prices, and buyer interest before and after Oct. 1, we focus on month-over-month changes and compare key metros to their regional and national aggregates.

One-month MoM snapshot (Sep → Oct 2025)

| Geography | New Listings | Page Views Per Property | Active Listings | Pending | Median List Price | Median List Price / SF | Median DOM |

|---|---|---|---|---|---|---|---|

| DC | -13.9% | -11.5% | 0.3% | 0.4% | -0.9% | -0.3% | 0 |

| VA Beach | -5.1% | -10.7% | -2.0% | -7.3% | -0.7% | -0.1% | 1 |

| Oklahoma City | -1.4% | -8.6% | 1.7% | -2.3% | -0.2% | -0.1% | 4 |

| Baltimore | -2.4% | -9.7% | 1.3% | -2.8% | -0.6% | -0.8% | 3 |

| South | 1.6% | -5.9% | 0.3% | -3.6% | -0.9% | -0.6% | 0 |

| National Avg. | -2.7% | -6.2% | 0.0% | -3.3% | -0.2% | -0.8% | 1 |

Upshot: The shutdown seems to have pressed pause, not stop, on housing market activity. Homebuyers and sellers are likely delaying, rather than canceling, their home search or listing process. If the shutdown drags on, we’ll keep an eye on longer-term dynamics, especially in DC, where broader federal workforce challenges may weigh more heavily on the outlook.

Appendix: October 2025 Statistics

October 2025 Regional Statistics

| Region | Active Listings, YoY | New Listings, YoY | Median List Price | Median LP, YoY | Median LP / SF, YoY | Median DOM, YoY (days) | Price-Reduced Share | PRS, YoY (pp) |

|---|---|---|---|---|---|---|---|---|

| Northeast | 8.9% | 3.3% | $525,000 | 0.0% | 3.8% | 2 | 14.5% | 1.2 |

| Midwest | 12.2% | 4.8% | $315,000 | 0.8% | 1.1% | 2 | 20.2% | 2.1 |

| South | 17.0% | 5.2% | $385,000 | -0.9% | -1.4% | 5 | 21.3% | 1.7 |

| West | 17.4% | 4.2% | $599,450 | -2.6% | -1.6% | 8 | 21.5% | 1.6 |

| National Avg. | 15.3% | 5.1% | $424,200 | 0.4% | -0.5% | 5 | 20.2% | 1.6 |

October 2025 Housing Overview of the 50 Largest Metros

Selected rows shown below (full table available in the source article).

| Metro | Active Listing YoY | New Listing YoY | Median LP | Median LP YoY | Median LP / SF YoY | Median DOM YoY (days) | Price-Reduced Share | PRS YoY (pp) |

|---|---|---|---|---|---|---|---|---|

| Atlanta, GA | 16.6% | 0.1% | $415,000 | 0.9% | -0.9% | 8 | 24.0% | 1.4 |

| Austin, TX | 11.0% | 13.7% | $489,859 | -5.7% | -5.1% | 7 | 26.7% | 2.5 |

| Baltimore, MD | 26.2% | -12.0% | $382,500 | 3.4% | 1.8% | 5 | 20.3% | 4.1 |

| Boston, MA–NH | 19.0% | -0.5% | $799,900 | -4.5% | -0.3% | 3 | 22.6% | 4.6 |

| Charlotte, NC–SC | 36.5% | 19.4% | $438,348 | 2.1% | -0.3% | 7 | 27.1% | 4.3 |

| Chicago, IL–IN–WI | -1.8% | -4.8% | $364,900 | -1.4% | 0.0% | 1 | 17.0% | 1.2 |

| Cincinnati, OH–KY–IN | 16.7% | 6.9% | $339,950 | 3.0% | 2.4% | 1 | 22.9% | 2.4 |

| Cleveland, OH | 11.7% | 3.6% | $259,900 | 4.0% | 4.0% | 1 | 21.2% | 1.9 |

| New York–Newark–Jersey City, NY–NJ | 3.9% | 7.2% | $762,450 | -1.6% | -3.5% | 1 | 9.6% | 0.6 |

| Oklahoma City, OK | 14.5% | 1.7% | $319,400 | 2.3% | 0.1% | 8 | 23.8% | -1.5 |

| Orlando, FL | 10.5% | -7.1% | $419,990 | -1.6% | -2.6% | 12 | 23.1% | -0.4 |

| Philadelphia, PA–NJ–DE–MD | 10.5% | -0.2% | $379,973 | 1.3% | 0.9% | -1 | 18.3% | 2.3 |

| Phoenix, AZ | 23.4% | 6.5% | $495,000 | -4.7% | -2.3% | 7 | 29.4% | 0.7 |

| Portland, OR–WA | 13.6% | -6.0% | $599,000 | -0.6% | -1.8% | 10 | 30.9% | 1.9 |

| Providence, RI–MA | 11.9% | 0.0% | $582,450 | 5.0% | 3.3% | 0 | 15.1% | -3.9 |

| Raleigh, NC | 30.6% | 9.7% | $458,020 | 0.2% | -0.7% | 9 | 25.4% | 7.5 |

| Richmond, VA | 22.8% | 7.5% | $429,000 | -2.5% | 0.8% | 4 | 18.3% | 2.9 |

| Riverside–San Bernardino, CA | 10.9% | 2.1% | $595,422 | -0.6% | -0.7% | 8 | 17.0% | -0.1 |

| Sacramento, CA | 14.8% | -3.2% | $610,000 | -2.8% | -1.9% | 9 | 21.8% | 2.5 |

| St. Louis, MO–IL | 11.8% | 9.0% | $295,900 | -1.2% | 3.3% | -1 | 19.4% | 2.0 |

| San Antonio, TX | 18.4% | N/A | $329,000 | -1.8% | -3.1% | 4 | 26.5% | 2.0 |

| San Diego, CA | 12.6% | N/A | $927,000 | -5.1% | -2.6% | 5 | 18.1% | 0.3 |

| San Francisco, CA | 2.3% | -1.8% | $954,500 | -4.0% | -4.2% | 4 | 15.4% | 0.7 |

| San Jose, CA | 9.5% | -6.0% | $1,381,500 | -0.9% | -1.4% | 5 | 15.1% | 2.0 |

| Seattle, WA | 28.1% | 5.5% | $762,343 | 0.6% | -0.2% | 4 | 22.1% | 3.9 |

| Tampa, FL | 17.9% | -4.5% | $409,000 | 2.3% | 1.0% | 7 | 26.7% | 1.7 |

| Tucson, AZ | 20.8% | 10.9% | $385,000 | -1.9% | -1.9% | 7 | 23.7% | 3.7 |

| Virginia Beach, VA–NC | 10.3% | 1.6% | $407,000 | 2.9% | 2.6% | 1 | 22.2% | 1.5 |

| Washington, DC–VA–MD–WV | 38.2% | -8.4% | $594,500 | -0.8% | -4.0% | 4 | 18.6% | 3.9 |

* Note: Changes in the underlying source data for the Washington, DC, Philadelphia, and Baltimore metro areas might mean that growth in active and new listings counts is slightly overstated or understated, depending on the season, and time on the market is slightly lower in 2025 relative to previous years. Unfortunately, there is no adjustment mechanism for these changes, and data trends should be viewed with caution.

With the release of its January 2025 housing trends report, Realtor.com® has restated data points for some previous months. As a result, some data released since January 2025 will not be directly comparable with previous data releases and research reports.

Reprinted in full with permission from Realtor.com® Research.

Original: October 2025 Monthly Housing Market Trends Report.

All images and charts © Realtor.com®; embedded via their public CDN links.

Share this post

Prepared by Broker★Agent Advisor

Advice, Recognition, and Referral since 1996